Buying a home is a dream for many, but with rising property prices, purchasing a home often requires financial assistance in the form of a home loan. At Best Growth Partners(realesta8.com), we understand that applying for a home loan can be a complex process. Our goal is to simplify it for you with this step-by-step guide.

Why Opt for a Home Loan?

A home loan offers financial support to buy your dream house without liquidating your savings. With competitive interest rates and long repayment tenures, it’s a practical option for most homebuyers. Here are some key benefits:

- Tax Benefits: You can claim deductions on both principal and interest components under sections 80C and 24(b) of the Income Tax Act.

- Flexible Tenure: Most banks offer repayment tenures ranging from 10 to 30 years.

- Ownership Advantage: Investing in a home builds a valuable asset for the future.

Step 1: Determine Your Home Loan Eligibility

Your eligibility for a home loan is determined by factors such as your income, age, employment status, and credit score. Lenders generally consider the following:

- Age Limit: 21 to 60 years for salaried individuals and up to 65 years for self-employed individuals.

- Employment Status: Minimum two years of stable employment or business history.

- Credit Score: A score above 750 increases your chances of approval.

Tip: Check your credit score before applying for a loan. A higher score can help you secure a lower interest rate.

Step 2: Research Different Lenders

It’s essential to compare different banks and financial institutions to find the best home loan offer. Look for factors such as:

- Interest Rates: Fixed vs. floating rates.

- Processing Fees: Usually 0.5% to 1% of the loan amount.

- Prepayment Charges: Some lenders charge fees for early repayment.

- Loan Tenure: Choose a tenure that suits your repayment capacity.

At Best Growth Partners, we assist our clients in comparing different lenders to make an informed decision.

Step 3: Calculate Your Loan Amount and EMI

Before applying for a home loan, calculate how much you need and assess your ability to repay. Use online EMI calculators to estimate your monthly installments.

Factors to consider:

- Loan Amount: Based on property value and your eligibility.

- Down Payment: Usually 10-25% of the property value.

- EMI: Should ideally be less than 40% of your monthly income.

Pro Tip: Keep some buffer for other expenses like registration, stamp duty, and furnishing.

Step 4: Prepare Required Documentation

Lenders require a set of documents for home loan approval. Here’s a checklist:

For Salaried Individuals:

- ID Proof (Aadhaar, PAN, Passport)

- Address Proof (Utility Bills, Rent Agreement)

- Salary Slips (Last 3 Months)

- Bank Statements (Last 6 Months)

- Form 16 or Income Tax Returns

For Self-Employed Individuals:

- ID and Address Proof

- Business Proof (Registration, GST)

- Bank Statements (Last 12 Months)

- Income Tax Returns (Last 3 Years)

- Profit & Loss Statement

Having all documents ready speeds up the process.

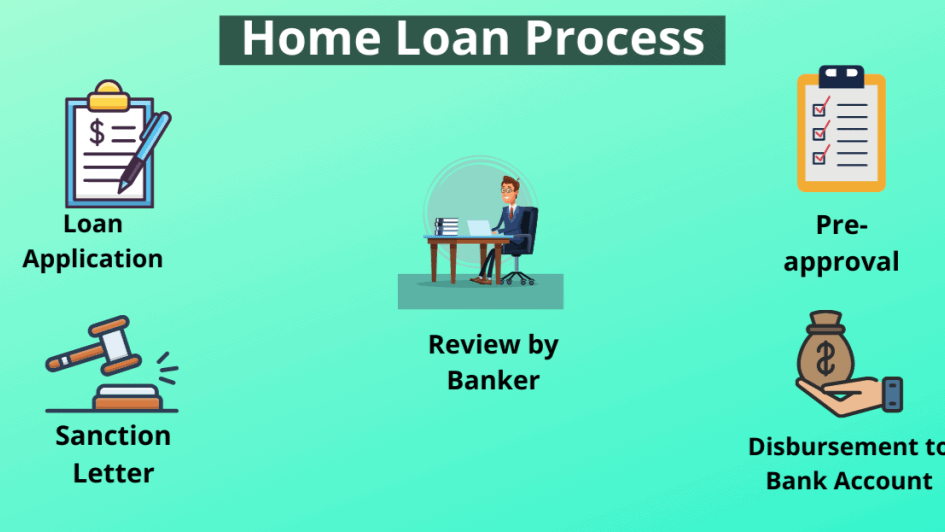

Step 5: Apply for the Home Loan

You can apply for a home loan online or by visiting the lender’s branch. Here’s how:

- Online Application:

- Offline Application:

At Best Growth Partners, we offer personalized assistance to help you navigate the application process efficiently.

Step 6: Verification and Approval Process

Once the application is submitted, the lender verifies your documents and assesses your creditworthiness. This involves:

- Document Verification: Ensuring all documents are valid and complete.

- Credit Assessment: Evaluating your credit score and repayment capacity.

- Property Valuation: Verifying the property details and market value.

If all checks are satisfactory, the lender will approve the loan.

Step 7: Loan Disbursement

After loan approval, the lender will disburse the loan amount. This can be:

- Full Disbursement: For ready-to-move-in properties.

- Partial Disbursement: For under-construction properties.

The amount is usually transferred directly to the seller or builder’s account.

Tips to Increase Home Loan Approval Chances

- Improve Your Credit Score: Pay off existing debts and avoid new loans.

- Choose a Co-Applicant: A joint application with a spouse or family member increases eligibility.

- Maintain Stable Income: Ensure your income flow is steady and verifiable.

- Provide Complete Documentation: Incomplete documents can delay or reject your application.

Common Mistakes to Avoid

- Applying with a Low Credit Score: Wait until your score improves.

- Ignoring Loan Terms: Read the fine print carefully.

- Not Comparing Lenders: Always compare multiple offers.

Conclusion

Applying for a home loan in India doesn’t have to be overwhelming. With proper preparation and guidance from Best Growth Partners, you can secure the best home loan that suits your needs. We are here to assist you at every step, ensuring a hassle-free experience.

Let’s make your dream home a reality!